The mechanism is not as popular in New Zealand. Grant Thornton explains why that should change

In the last five years, the use of a locked box mechanism (LBM) for transaction completion has risen, but uptake has been slow in New Zealand.

Grant Thornton International’s research report, ‘A smarter way to get deals done’, reveals that 54% of New Zealand businesses surveyed had used LBM in 2017 on an estimated 8% of transactions, compared to 76% of international respondents that used the LBM on 41% of transactions.

The low usage of LBM in New Zealand is likely due to a lack of familiarity. But ambivalence shouldn’t deter potential buyers and sellers from using the method when negotiating Sale and Purchase Agreements (SPA).

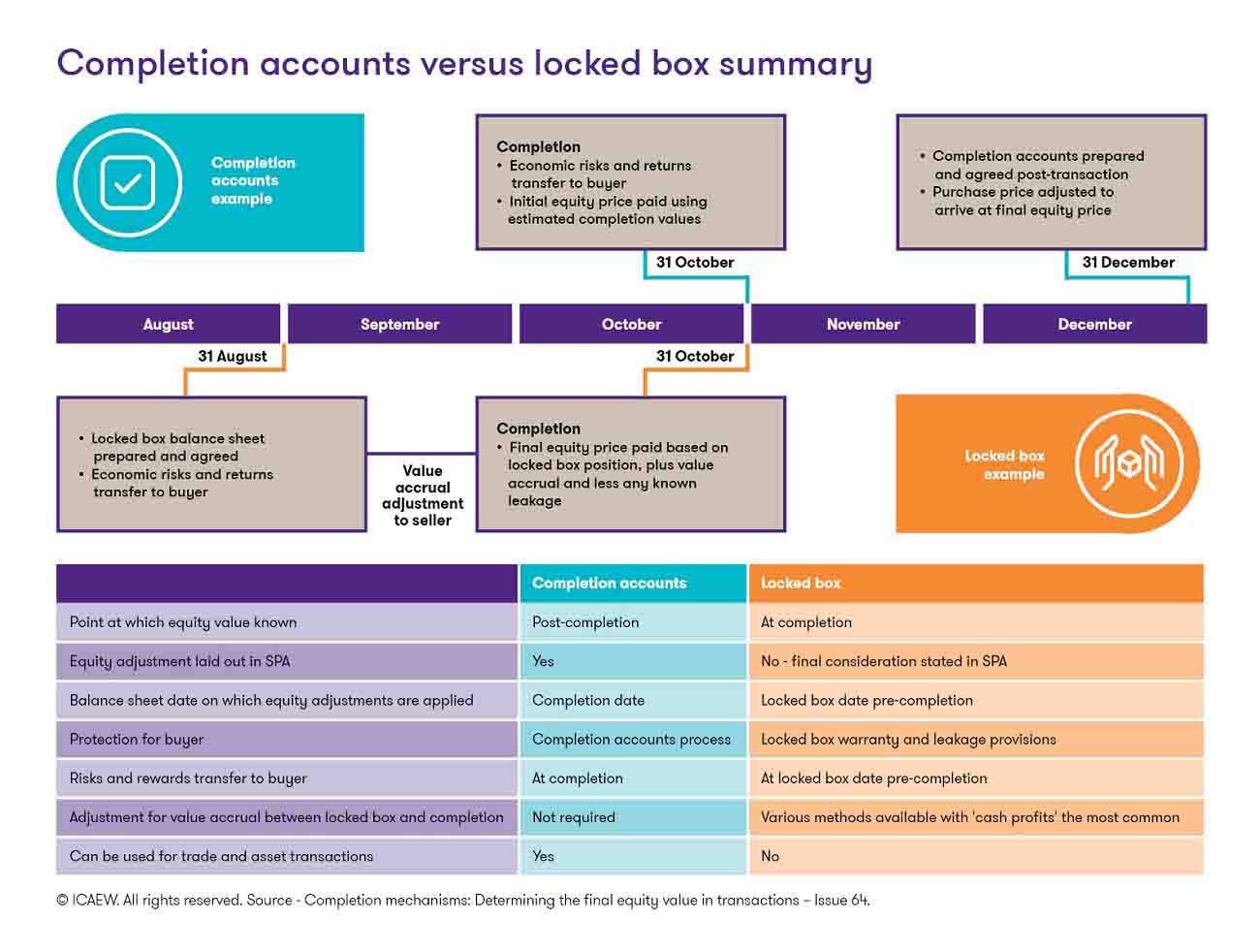

What is LBM?

In simple terms, LBM means the final equity value adjustments are applied to a balance sheet prepared at a date prior to completion, which is called the ‘locked box balance sheet’. The seller usually provides a warranty to the buyer for the accuracy of the locked box accounts which provides certainty to both the buyer and seller at the time of signing the SPA.

No value is permitted to leave the business between the locked box date until completion of the transaction. The agreed equity value adjustments are applied (i.e., a working capital adjustment) to the assets and liabilities at the locked box date; there are minimal further adjustments to take account of movements in value between locked box date and completion.

What are the benefits?

A locked box mechanism removes the need for completion accounts which often results in price adjustment disputes between buyers and sellers.

What about leakage?

LBM can leave the buyer open to manipulation of the seller’s financial position. To avoid this, the seller guarantees not to extract value from the target business in the period from the locked box date to completion, with the exception of narrowly defined items specifically agreed by the buyer and outlined in the SPA. This is often called “permitted leakage”, and can also cover transactions between the business and the seller such as agreed salary or management fees payable to the seller in this period.

Timing is also important. The absence of a post completion adjustment mechanism means a buyer should carry out rigorous due diligence on the locked box balance sheet to ensure it is accurate. The locked box date should not be too close to the completion date so there is enough time for the seller to prepare, and for the buyer to review it prior to completion. The locked box date should not be too far in the past because it will increase the risk of leakage and the actual profits being materially different from the value accrual. A commonly used date is the target group’s last financial year end.

Managing value movement

Economic risks and returns effectively transfer to the buyer at the locked box date.

However, a seller may still be managing the business to generate profit and will have capital tied up until the completion date when the consideration is paid. Sellers may therefore expect to be compensated for this via an upward adjustment to the consideration (assuming the business is profitable); this adjustment is often referred to as the ‘value accrual’.

One approach which is often used to calculate the value accrual is ‘cash profits’ which can be viewed as an estimate of the movement in value that would have been realised had a completion accounts mechanism been applied.

Capital expenditure is also normally included in the cash profits calculation (excluding any amounts already treated as debt-like items), though parties sometimes exclude capital expenditure that they agree is over and above-normal maintenance levels.

How are New Zealand businesses using LBM?

Grant Thornton’s research revealed when using the LBM, buyers and sellers in New Zealand typically use the ‘cash profits’ basis, or a debt or equity based interest rate to establish seller compensation between the locked box date and completion. However, 50% of respondents used no post locked box ticker, which could make the mechanism advantageous to a buyer when compared to the closing account mechanism.

Grant Thornton has been involved in several negotiations where no compensation was factored into the locked box for interim management by the seller until completion. However, interest rates were applicable if significant delays between locked box date and completion occurred.

Although the most popular price adjustment in New Zealand is still completion accounts, talk to a business advisor about the locked box mechanism. In theory, the choice of completion mechanism should not affect the final equity price paid for a business, but in practice, the result is likely to be different.

To read more about LBM and market practice for equity value and Sale and Purchase agreements, download our report, ‘A smarter way to get deals done’.

Russell Moore

National Managing Partner

Grant Thornton New Zealand

T: +64 9 922 1237

E: [email protected]

Richard Hughes

Associate Director, Financial Advisory Services

Grant Thornton New Zealand

T: +64 9 308 2570

E: [email protected]